All Categories

Featured

Table of Contents

The technique has its own advantages, yet it additionally has problems with high costs, complexity, and extra, leading to it being considered a fraud by some. Infinite financial is not the ideal policy if you require just the investment part. The infinite banking principle focuses on making use of whole life insurance policy plans as a financial tool.

A PUAR enables you to "overfund" your insurance plan right up to line of it coming to be a Customized Endowment Agreement (MEC). When you use a PUAR, you rapidly enhance your cash value (and your death advantage), thereby raising the power of your "bank". Further, the even more money value you have, the greater your interest and returns settlements from your insurer will certainly be.

With the surge of TikTok as an information-sharing platform, economic advice and strategies have actually found a novel means of dispersing. One such approach that has been making the rounds is the infinite banking principle, or IBC for short, garnering recommendations from celebrities like rapper Waka Flocka Flame - Wealth management with Infinite Banking. While the approach is presently preferred, its roots map back to the 1980s when economist Nelson Nash presented it to the globe.

What financial goals can I achieve with Infinite Banking Vs Traditional Banking?

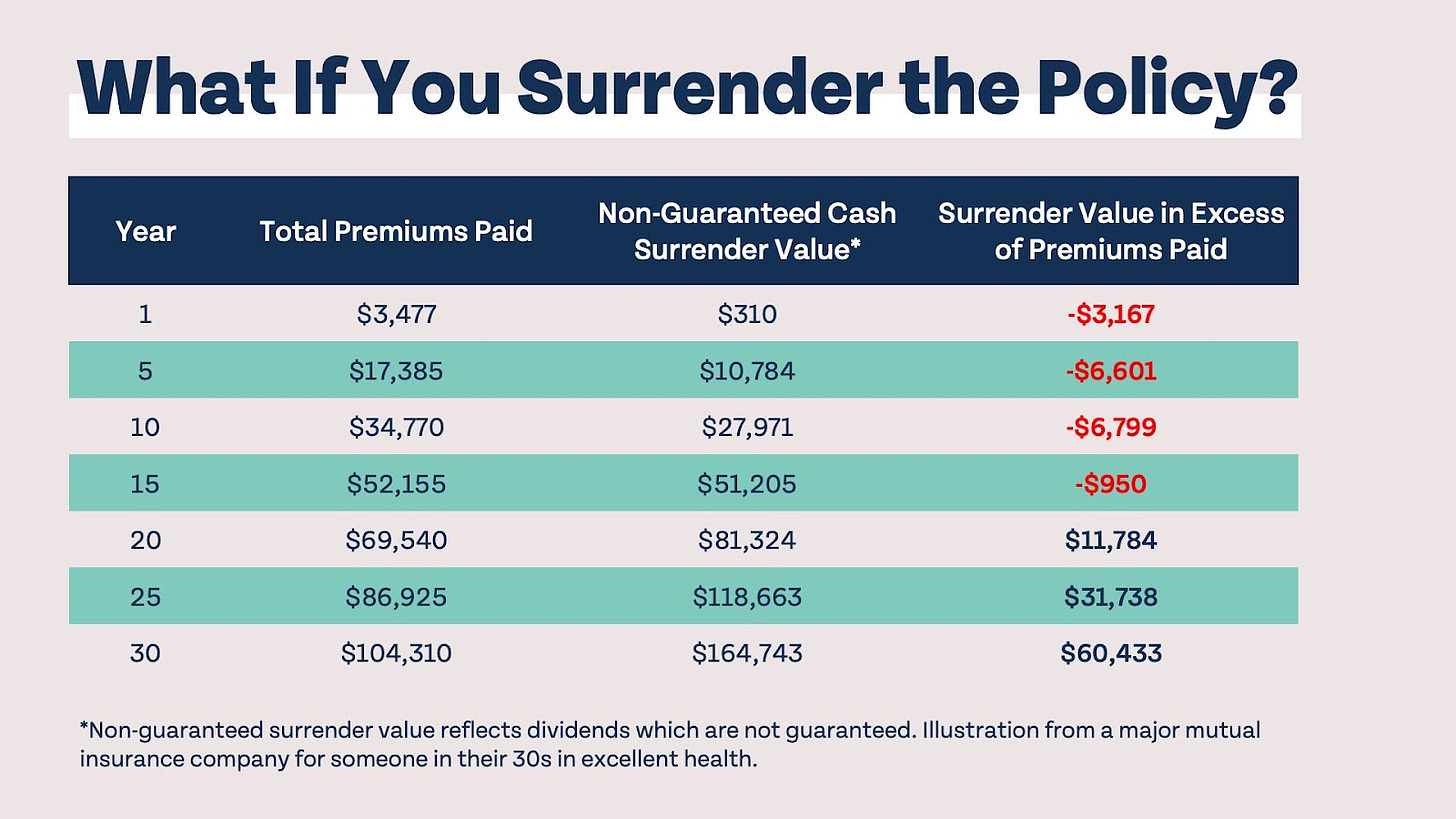

Within these policies, the money value expands based upon a rate established by the insurance firm. As soon as a significant cash value collects, insurance holders can obtain a money worth funding. These fundings differ from standard ones, with life insurance coverage working as collateral, suggesting one might shed their coverage if loaning exceedingly without adequate cash money worth to sustain the insurance coverage prices.

And while the allure of these plans is noticeable, there are inherent restrictions and risks, demanding persistent cash money value surveillance. The method's legitimacy isn't black and white. For high-net-worth people or local business owner, especially those making use of approaches like company-owned life insurance coverage (COLI), the benefits of tax obligation breaks and compound growth might be appealing.

The attraction of unlimited banking doesn't negate its challenges: Expense: The foundational requirement, a permanent life insurance policy policy, is costlier than its term counterparts. Qualification: Not every person qualifies for entire life insurance policy as a result of extensive underwriting processes that can exclude those with certain wellness or lifestyle problems. Intricacy and risk: The intricate nature of IBC, paired with its risks, might prevent several, particularly when easier and less dangerous choices are available.

Private Banking Strategies

Allocating around 10% of your monthly income to the plan is just not possible for the majority of people. Component of what you review below is just a reiteration of what has actually currently been claimed above.

So prior to you obtain right into a situation you're not prepared for, know the adhering to first: Although the idea is typically marketed because of this, you're not really taking a loan from yourself. If that were the case, you would not need to settle it. Rather, you're borrowing from the insurance provider and need to settle it with interest.

Some social media posts suggest making use of cash value from entire life insurance to pay down debt card debt. When you pay back the lending, a portion of that rate of interest goes to the insurance policy company.

What resources do I need to succeed with Wealth Building With Infinite Banking?

For the initial numerous years, you'll be paying off the commission. This makes it exceptionally challenging for your policy to accumulate value throughout this time around. Whole life insurance coverage expenses 5 to 15 times a lot more than term insurance coverage. The majority of people just can't afford it. Unless you can afford to pay a few to a number of hundred bucks for the following decade or even more, IBC will not function for you.

Not everybody ought to depend only on themselves for monetary safety and security. Borrowing against cash value. If you require life insurance coverage, here are some important tips to consider: Think about term life insurance. These policies offer protection throughout years with significant monetary responsibilities, like home mortgages, pupil finances, or when taking care of young youngsters. See to it to search for the best rate.

Can I use Cash Value Leveraging to fund large purchases?

Visualize never having to fret concerning financial institution lendings or high interest rates again. That's the power of infinite financial life insurance.

Through Infinite Banking, business owners eliminate reliance on banks. how to borrow against life insurance for infinite banking.

This strategy allows businesses to finance expansion without relying on high-interest loans.

Business finance specialists can optimize policies for maximum growth. Speak with an Infinite Banking professional today to take advantage of tax-free capital.

There's no set finance term, and you have the freedom to select the repayment schedule, which can be as leisurely as settling the car loan at the time of fatality. This flexibility encompasses the maintenance of the lendings, where you can opt for interest-only repayments, maintaining the finance equilibrium flat and convenient.

Infinite Banking For Financial Freedom

Holding money in an IUL fixed account being credited interest can commonly be far better than holding the cash money on down payment at a bank.: You've constantly fantasized of opening your own pastry shop. You can obtain from your IUL plan to cover the initial expenses of renting out a room, acquiring tools, and employing staff.

Personal fundings can be gotten from standard banks and cooperative credit union. Here are some bottom lines to consider. Bank card can offer a flexible means to borrow cash for really temporary periods. Nonetheless, borrowing money on a credit card is typically extremely pricey with annual percent prices of rate of interest (APR) typically reaching 20% to 30% or more a year.

{kind=link}

Latest Posts

Bank On Yourself Insurance Companies

Becoming Your Own Banker Nelson Nash Pdf

Be Your Own Banker Whole Life Insurance